{“page”:0,” year”:2023,” monthnum”:11,” day”:28,” name”:” the-gold-standard-of-indices-meets-todays-technology”,” mistake”:””,” m”:””,” p”:0,” post_parent”:””,” subpost”:””,” subpost_id”:””,” accessory”:””,” attachment_id”:0,” pagename”:””,” page_id”:0,” 2nd”:””,” minute”:””,” hour”:””,” w”:0,” category_name”:””,” tag”:””,” feline”:””,” tag_id”:””,” author”:””,” author_name”:””,” feed”:””,” tb”:””,” paged”:0,” meta_key”:””,” meta_value”:””,” sneak peek”:””,” s”:””,” sentence”:””,” title”:””,” fields”:””,” menu_order”:””,” embed”:””,” classification __ in”: [],” classification __ not_in”: [],” classification __ and”: [],” post __ in”: [],” post __ not_in”: [],” post_name __ in”: [],” tag __ in”: [],” tag __ not_in”: [],” tag __ and”: [],” tag_slug __ in”: [],” tag_slug __ and”: [],” post_parent __ in”: [],” post_parent __ not_in”: [],” author __ in”: [],” author __ not_in”: [],” search_columns”: [],” ignore_sticky_posts”: incorrect,” suppress_filters”: incorrect,” cache_results”: real,” update_post_term_cache”: real,” update_menu_item_cache”: incorrect,” lazy_load_term_meta”: real,” update_post_meta_cache”: real,” post_type”:””,” posts_per_page”:” 5″,” nopaging”: incorrect,” comments_per_page”:” 50″,” no_found_rows”: incorrect,” order”:” DESC”}

[{“display”:”Craig Lazzara”,”title”:”Managing Director, Index Investment Strategy”,”image”:”/wp-content/authors/craig_lazzara-353.jpg”,”url”:”https://www.indexologyblog.com/author/craig_lazzara/”},{“display”:”Tim Edwards”,”title”:”Managing Director, Index Investment Strategy”,”image”:”/wp-content/authors/timothy_edwards-368.jpg”,”url”:”https://www.indexologyblog.com/author/timothy_edwards/”},{“display”:”Hamish Preston”,”title”:”Head of U.S. Equities”,”image”:”/wp-content/authors/hamish_preston-512.jpg”,”url”:”https://www.indexologyblog.com/author/hamish_preston/”},{“display”:”Anu Ganti”,”title”:”Senior Director, Index Investment Strategy”,”image”:”/wp-content/authors/anu_ganti-505.jpg”,”url”:”https://www.indexologyblog.com/author/anu_ganti/”},{“display”:”Fiona Boal”,”title”:”Managing Director, Global Head of Equities”,”image”:”/wp-content/authors/fiona_boal-317.jpg”,”url”:”https://www.indexologyblog.com/author/fiona_boal/”},{“display”:”Jim Wiederhold”,”title”:”Director, Commodities and Real Assets”,”image”:”/wp-content/authors/jim.wiederhold-515.jpg”,”url”:”https://www.indexologyblog.com/author/jim-wiederhold/”},{“display”:”Phillip Brzenk”,”title”:”Managing Director, Global Head of Multi-Asset Indices”,”image”:”/wp-content/authors/phillip_brzenk-325.jpg”,”url”:”https://www.indexologyblog.com/author/phillip_brzenk/”},{“display”:”Howard Silverblatt”,”title”:”Senior Index Analyst, Product Management”,”image”:”/wp-content/authors/howard_silverblatt-197.jpg”,”url”:”https://www.indexologyblog.com/author/howard_silverblatt/”},{“display”:”John Welling”,”title”:”Director, Global Equity Indices”,”image”:”/wp-content/authors/john_welling-246.jpg”,”url”:”https://www.indexologyblog.com/author/john_welling/”},{“display”:”Michael Orzano”,”title”:”Senior Director, Global Equity Indices”,”image”:”/wp-content/authors/Mike.Orzano-231.jpg”,”url”:”https://www.indexologyblog.com/author/mike-orzano/”},{“display”:”Wenli Bill Hao”,”title”:”Senior Lead, Factors and Dividends Indices, Product Management and Development”,”image”:”/wp-content/authors/bill_hao-351.jpg”,”url”:”https://www.indexologyblog.com/author/bill_hao/”},{“display”:”Maria Sanchez”,”title”:”Director, Sustainability Index Product Management, U.S. Equity Indices”,”image”:”/wp-content/authors/maria_sanchez-527.jpg”,”url”:”https://www.indexologyblog.com/author/maria_sanchez/”},{“display”:”Shaun Wurzbach”,”title”:”Managing Director, Head of Commercial Group (North America)”,”image”:”/wp-content/authors/shaun_wurzbach-200.jpg”,”url”:”https://www.indexologyblog.com/author/shaun_wurzbach/”},{“display”:”Silvia Kitchener”,”title”:”Director, Global Equity Indices, Latin America”,”image”:”/wp-content/authors/silvia_kitchener-522.jpg”,”url”:”https://www.indexologyblog.com/author/silvia_kitchener/”},{“display”:”Akash Jain”,”title”:”Director, Global Research & Design”,”image”:”/wp-content/authors/akash_jain-348.jpg”,”url”:”https://www.indexologyblog.com/author/akash_jain/”},{“display”:”Ved Malla”,”title”:”Associate Director, Client Coverage”,”image”:”/wp-content/authors/ved_malla-347.jpg”,”url”:”https://www.indexologyblog.com/author/ved_malla/”},{“display”:”Rupert Watts”,”title”:”Head of Factors and Dividends”,”image”:”/wp-content/authors/rupert_watts-366.jpg”,”url”:”https://www.indexologyblog.com/author/rupert_watts/”},{“display”:”Jason Giordano”,”title”:”Director, Fixed Income, Product Management”,”image”:”/wp-content/authors/jason_giordano-378.jpg”,”url”:”https://www.indexologyblog.com/author/jason_giordano/”},{“display”:”Sherifa Issifu”,”title”:”Senior Analyst, U.S. Equity Indices”,”image”:”/wp-content/authors/sherifa_issifu-518.jpg”,”url”:”https://www.indexologyblog.com/author/sherifa_issifu/”},{“display”:”Qing Li”,”title”:”Director, Global Research & Design”,”image”:”/wp-content/authors/qing_li-190.jpg”,”url”:”https://www.indexologyblog.com/author/qing_li/”},{“display”:”Brian Luke”,”title”:”Senior Director, Head of Commodities, Real & Digital Assets”,”image”:”/wp-content/authors/brian.luke-509.jpg”,”url”:”https://www.indexologyblog.com/author/brian-luke/”},{“display”:”Glenn Doody”,”title”:”Vice President, Product Management, Technology Innovation and Specialty Products”,”image”:”/wp-content/authors/glenn_doody-517.jpg”,”url”:”https://www.indexologyblog.com/author/glenn_doody/”},{“display”:”Priscilla Luk”,”title”:”Managing Director, Global Research & Design, APAC”,”image”:”/wp-content/authors/priscilla_luk-228.jpg”,”url”:”https://www.indexologyblog.com/author/priscilla_luk/”},{“display”:”Sean Freer”,”title”:”Director, Global Equity Indices”,”image”:”/wp-content/authors/sean_freer-490.jpg”,”url”:”https://www.indexologyblog.com/author/sean_freer/”},{“display”:”Liyu Zeng”,”title”:”Director, Global Research & Design”,”image”:”/wp-content/authors/liyu_zeng-252.png”,”url”:”https://www.indexologyblog.com/author/liyu_zeng/”},{“display”:”George Valantasis”,”title”:”Associate Director, Factors and Dividends”,”image”:”/wp-content/authors/george-valantasis-453.jpg”,”url”:”https://www.indexologyblog.com/author/george-valantasis/”},{“display”:”Barbara Velado”,”title”:”Senior Analyst, Research & Design, Sustainability Indices”,”image”:”/wp-content/authors/barbara_velado-413.jpg”,”url”:”https://www.indexologyblog.com/author/barbara_velado/”},{“display”:”Cristopher Anguiano”,”title”:”Senior Analyst, U.S. Equity Indices”,”image”:”/wp-content/authors/cristopher_anguiano-506.jpg”,”url”:”https://www.indexologyblog.com/author/cristopher_anguiano/”},{“display”:”Benedek Vu00f6ru00f6s”,”title”:”Director, Index Investment Strategy”,”image”:”/wp-content/authors/benedek_voros-440.jpg”,”url”:”https://www.indexologyblog.com/author/benedek_voros/”},{“display”:”Michael Mell”,”title”:”Global Head of Custom Indices”,”image”:”/wp-content/authors/michael_mell-362.jpg”,”url”:”https://www.indexologyblog.com/author/michael_mell/”},{“display”:”Joseph Nelesen”,”title”:”Senior Director, Index Investment Strategy”,”image”:”/wp-content/authors/joseph_nelesen-452.jpg”,”url”:”https://www.indexologyblog.com/author/joseph_nelesen/”},{“display”:”Maya Beyhan”,”title”:”Senior Director, ESG Specialist, Index Investment Strategy”,”image”:”/wp-content/authors/maya.beyhan-480.jpg”,”url”:”https://www.indexologyblog.com/author/maya-beyhan/”},{“display”:”Andrew Innes”,”title”:”Head of EMEA, Global Research & Design”,”image”:”/wp-content/authors/andrew_innes-189.jpg”,”url”:”https://www.indexologyblog.com/author/andrew_innes/”},{“display”:”Fei Wang”,”title”:”Senior Analyst, U.S. Equity Indices”,”image”:”/wp-content/authors/fei_wang-443.jpg”,”url”:”https://www.indexologyblog.com/author/fei_wang/”},{“display”:”Rachel Du”,”title”:”Senior Analyst, Global Research & Design”,”image”:”/wp-content/authors/rachel_du-365.jpg”,”url”:”https://www.indexologyblog.com/author/rachel_du/”},{“display”:”Izzy Wang”,”title”:”Senior Analyst, Factors and Dividends”,”image”:”/wp-content/authors/izzy.wang-326.jpg”,”url”:”https://www.indexologyblog.com/author/izzy-wang/”},{“display”:”Jason Ye”,”title”:”Director, Factors and Thematics Indices”,”image”:”/wp-content/authors/Jason%20Ye-448.jpg”,”url”:”https://www.indexologyblog.com/author/jason-ye/”},{“display”:”Jaspreet Duhra”,”title”:”Managing Director, Global Head of Sustainability Indices”,”image”:”/wp-content/authors/jaspreet_duhra-504.jpg”,”url”:”https://www.indexologyblog.com/author/jaspreet_duhra/”},{“display”:”Eduardo Olazabal”,”title”:”Senior Analyst, Global Equity Indices”,”image”:”/wp-content/authors/eduardo_olazabal-451.jpg”,”url”:”https://www.indexologyblog.com/author/eduardo_olazabal/”},{“display”:”Srineel Jalagani”,”title”:”Senior Director, Thematic Indices”,”image”:”/wp-content/authors/srineel_jalagani-446.jpg”,”url”:”https://www.indexologyblog.com/author/srineel_jalagani/”},{“display”:”Ari Rajendra”,”title”:”Senior Director, Head of Thematic Indices”,”image”:”/wp-content/authors/Ari.Rajendra-524.jpg”,”url”:”https://www.indexologyblog.com/author/ari-rajendra/”},{“display”:”Louis Bellucci”,”title”:”Senior Director, Index Governance”,”image”:”/wp-content/authors/louis_bellucci-377.jpg”,”url”:”https://www.indexologyblog.com/author/louis_bellucci/”},{“display”:”Daniel Perrone”,”title”:”Director and Head of Operations, ESG Indices”,”image”:”/wp-content/authors/daniel_perrone-387.jpg”,”url”:”https://www.indexologyblog.com/author/daniel_perrone/”},{“display”:”Elizabeth Bebb”,”title”:”Director, Factor & Dividend Indices”,”image”:”/wp-content/authors/elizabeth_bebb-511.jpg”,”url”:”https://www.indexologyblog.com/author/elizabeth_bebb/”},{“display”:”Raghu Ramachandran”,”title”:”Head of Insurance Asset Channel”,”image”:”/wp-content/authors/raghu_ramachandram-288.jpg”,”url”:”https://www.indexologyblog.com/author/raghu_ramachandram/”}]

The Gold Requirement of Indices Meet’s Today’s Innovation

Satisfy the S&P 500 FC Index, an ingenious index created to change allotments based upon intraday volatility signals as it looks for to increase stability, limitation direct exposure to drawdowns, while enhancing direct exposure to the S&P 500 by means of BofA’s Quick Merging innovation.

The posts on this blog site are viewpoints, not recommendations. Please read our Disclaimers

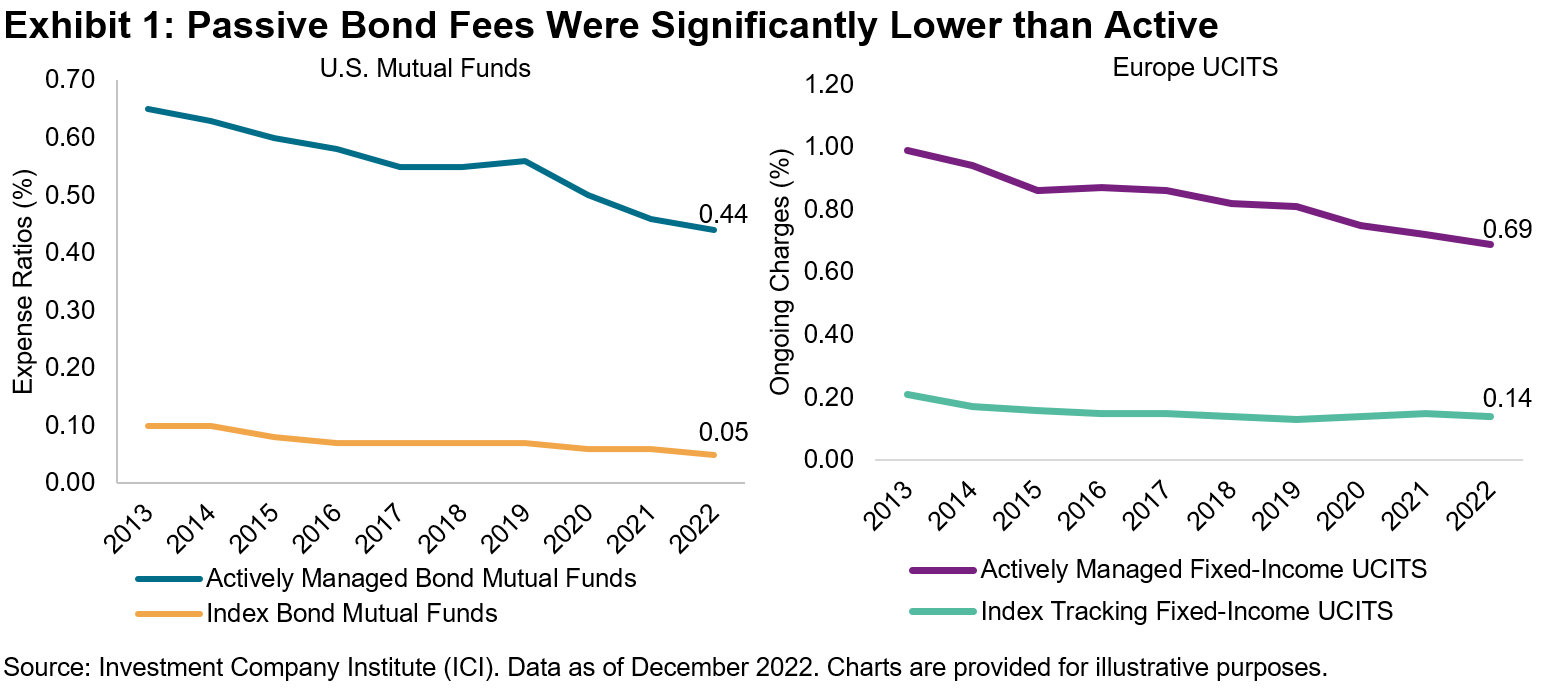

Finding Charge Cost Savings in Fixed Earnings

Among the advantages of indexing is its low expense relative to active management. As indexing has actually grown, financiers have actually benefited significantly by minimizing costs and preventing active underperformance. These advantages are not restricted simply to equities however have actually likewise encompassed other possession classes consisting of the set earnings area, where costs can play an especially essential function

In Exhibition 1, we see that index mutual fund costs in the U.S. and Europe have actually been regularly lower than their active equivalents for the previous years. While that spread has actually narrowed in the last few years, we still observe a cost differential of 39 bps in the U.S. and 55 bps in Europe since 2022.

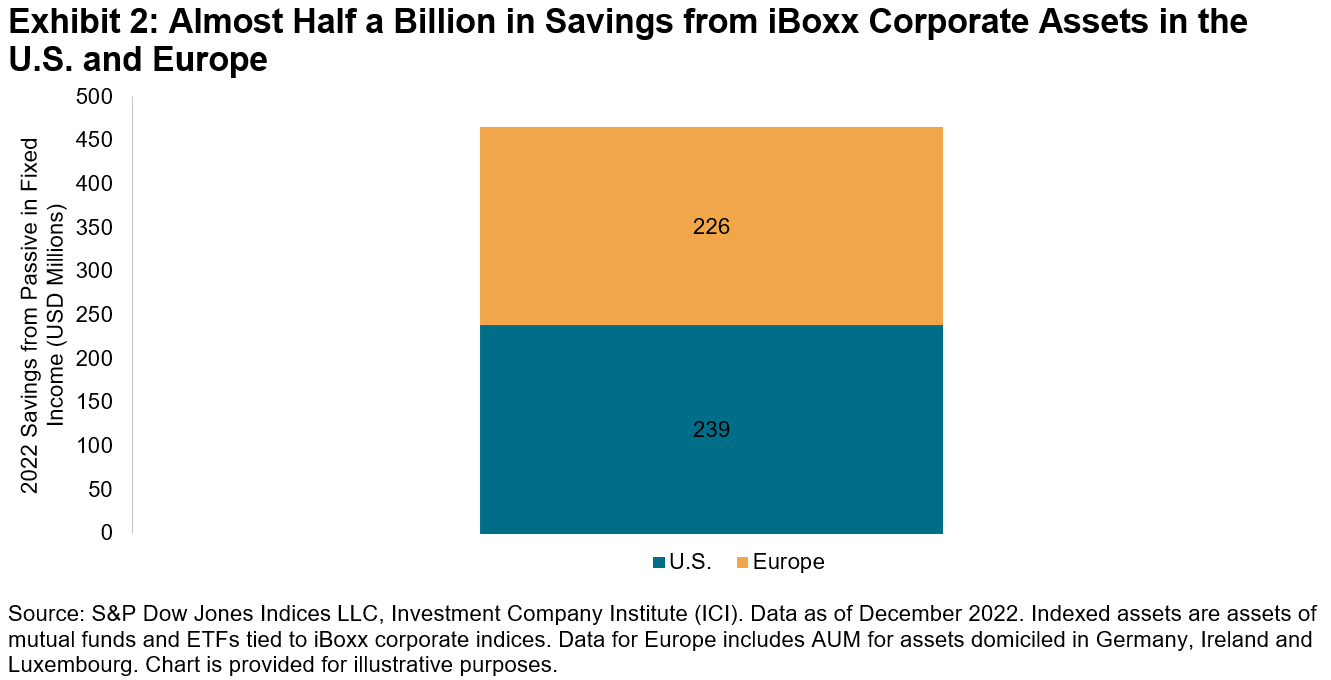

Utilizing the very same typical charge differentials in between active and passive set earnings funds in the U.S. and Europe, as used regionally to roughly USD 102 billion of possessions purchased shared funds and ETFs tracking iBoxx business bond indices in both areas, we can approximate an existing run rate of equivalent to a minimum of USD 465 million annually in charge cost savings made by passive financiers thanks in part to the iBoxx series (see Exhibition 2).

Obviously, this USD 465 million quote downplays the complete expense savings of the set earnings index market, because it includes funds tracking just choose indices from S&P Dow Jones Indices in the U.S. and Europe.

Our Yearly Study of Indexed Properties programs international possessions tracking our iBoxx Corporate indices were USD 121 billion since December 2022 (this likewise consists of institutional segregated requireds, along with possessions outside the U.S. and Europe). To offer context on the size of the passive market in set earnings, this number comprises just 1% of the international overall of USD 11.5 trillion in possessions of all open-end mutual fund 1 and just around 0.5% of international ranked business financial obligation exceptional. 2 Simply put, there is lots of headroom for future passive development in set earnings, and the potential customers for higher charge cost savings are appealing.

Certainly, the cost savings produced by the shift from active to passive management would be of no alleviation if financiers lost more in efficiency shortages than they got in lowered costs. As readers of our SPIVA ®(* )reports might understand, in the 15 years ending in June 2023, 94% of all actively handled General Financial investment Grade mutual fund lagged the iBoxx $ Liquid Financial investment Grade Index High Yield outcomes were practically similarly frustrating. As indexing in set earnings has actually gotten momentum, bond market individuals have actually gained from charge cost savings and avoidance of active underperformance, an effective mix. 1

2023 Investment Firm Reality Book , Investment Firm Institute. Controlled open-end funds consist of shared funds, exchange-traded funds (ETFs) and institutional funds. 2

Credit Trends: Global State of Play: Financial Obligation Development Diverging by Credit Quality. Level of international ranked business financial obligation reached USD 23.2 trillion since July 1, 2023. The posts on this blog site are viewpoints, not recommendations. Please read our

The

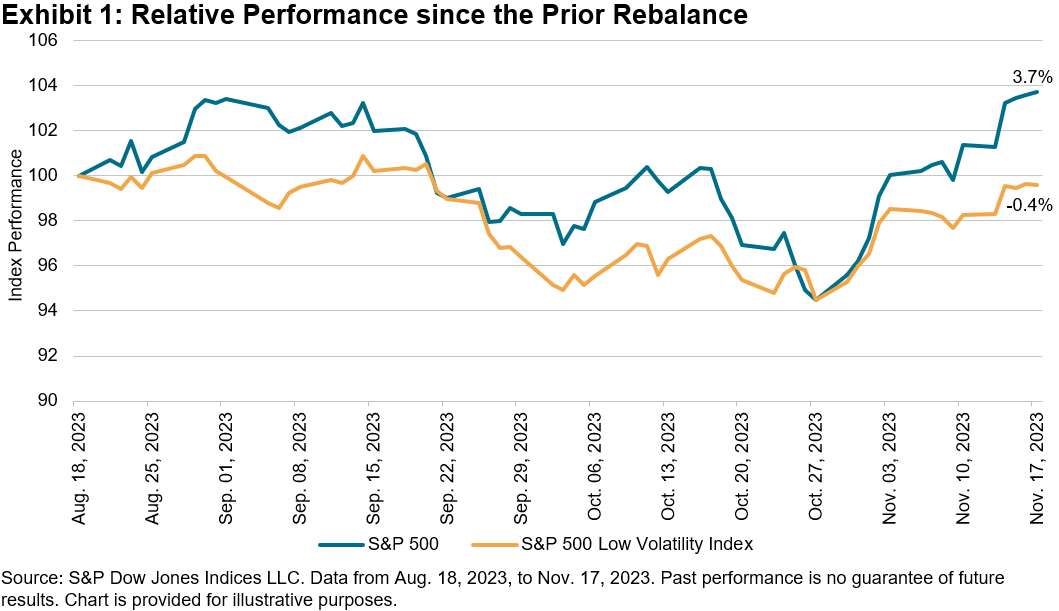

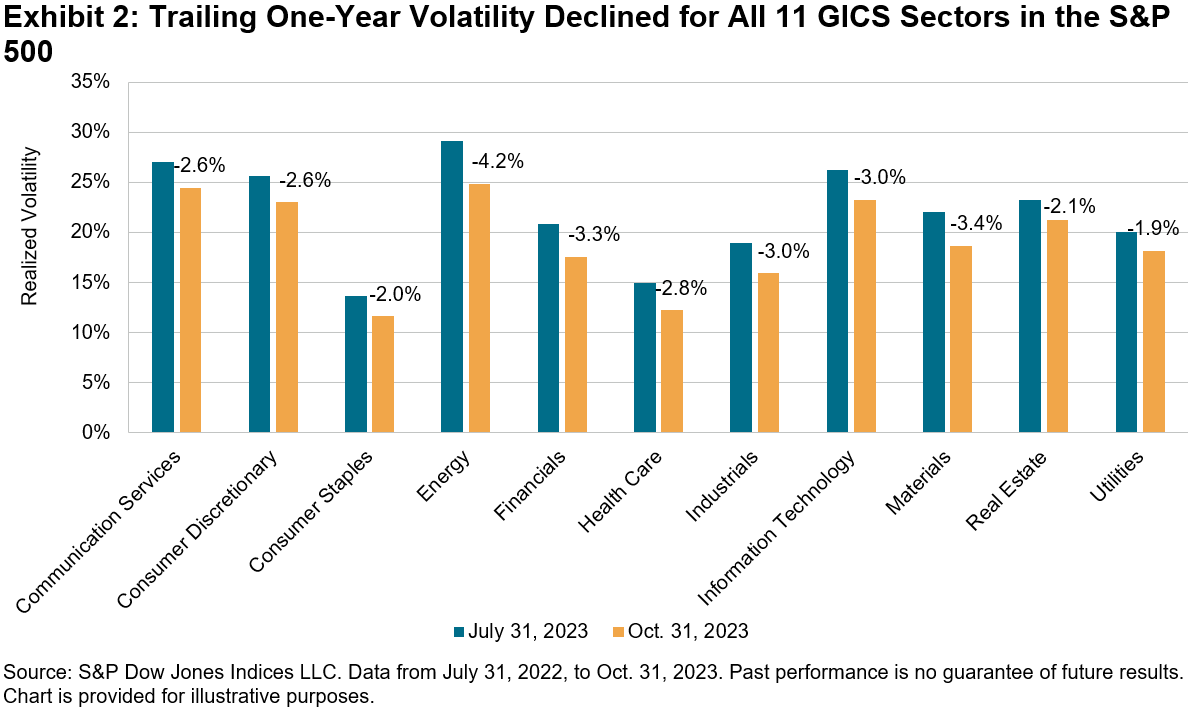

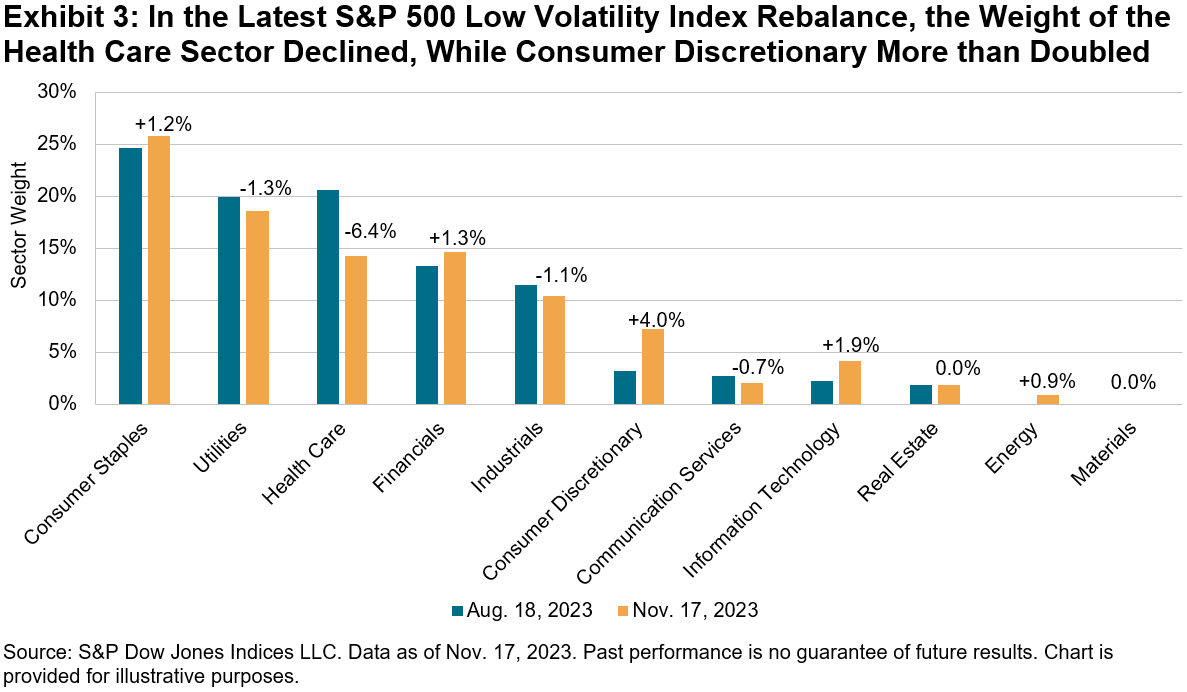

S&P 500 ®(* )continued its strong efficiency this year after publishing a 9.8% gain in a period of less than 3 weeks from Oct. 30 to Nov. 17, 2023. Throughout this duration, the 10-year U.S. Treasury yield dropped roughly 45 bps 1 and October’s year-over-year heading CPI inflation cooled to 3.2%. 2 As Exhibition 1 reveals, because the previous rebalance for the S&P 500 Low Volatility Index on Aug. 18, 2023, through the most current rebalance on Nov. 17, 2023, the S&P 500 was up 3.7%, versus a decrease of 0.4% for the S&P 500 Low Volatility Index. This kind of divergence can occur specifically throughout durations of strong efficiency and low volatility for the S&P 500. Throughout this duration, the annualized everyday basic variance for the S&P 500 was a fairly low 13.6%. As Exhibition 2 programs, the tracking 1 year volatility reduced for all 11 GICS sectors from July 31, 2023, to Oct. 31, 2023. The extensive decrease in volatility throughout all 11 GICS sectors followed the very same pattern in the 3 months prior to this duration. Determined in outright terms, volatility reduced the most for the Energy sector, although it stayed the most unstable sector at 24.9%. Since Oct. 31, 2023, Customer Staples was the least unstable sector, with an everyday understood volatility of just 11.6%. In the middle of the general reduction in volatility, the current rebalance of the S&P 500 Low Volatility Index brought some product modifications to sector weightings, most significantly in the Healthcare and Customer Discretionary sectors.

Following the most current rebalance, Healthcare’s weight visited 6.4%. Around 4.0% moved to the Customer Discretionary sector, more than doubling its weight to 7.3%. Other noteworthy receivers were the Infotech sector, which saw its weight practically double from 2.3% to 4.2%, along with the Customer Staples sector, which increased its weight to 26%.

After the Energy sector got a little allotment of roughly 1%, the Products sector is now the only sector without any allotment in the S&P 500 Low Volatility Index. The most recent rebalance ended up being reliable after the marketplace close on Nov. 17, 2023.

1

https://fred.stlouisfed.org/series/DGS10

2 https://www.bls.gov/news.release/cpi.nr0.htm

The posts on this blog site are viewpoints, not recommendations. Please read our Disclaimers

A Tactical Take A Look At Sectors Classifications

Equities

-

Tags

Anu Ganti, -

dispersion,

energy, GICS sectors, indexing sectors, liquidity, sector rotation, Select sector ETFs, choose sectors, Tactical Methods, United States FA How are consultants utilizing sector information to comprehend market patterns and notify financial investment choices? S&P DJI’s Anu Ganti signs up with Fairlead Methods’ Katie Stockton to talk about useful applications for sector indices. https://www.youtube.com/watch?v=9-MWc43uvRk

Senior Director, Index Financial Investment Technique

® Leading 50 outmatching the S&P SmallCap 600 ® by 30% YTD. 1 As an outcome of its fundamental small-cap predisposition, the S&P 500 Equal Weight Index (EWI) has actually suffered appropriately, underperforming the S&P 500 by 11% in the twelve months through October However as we observe from the troughs and peaks in Exhibition 1, Equal Weight has actually constantly handled to recuperate from deep losses. February 2001, February 2010 and March 2021 are 3 prime examples, post significant occasions like the tech bubble, monetary crisis and COVID-19 economic downturn. While the technique has actually deteriorated up until now this year,

we understand from Exhibition 2 that Equal Weight tends to surpass over the long term The technique’s little size, anti-momentum and worth tilts are crucial efficiency factors. Even More, Equal Weight’s natural rebalancing system of offering the winners and purchasing the losers is a crucial advantage of the mean reversion we observe in Exhibition 1. The predicament at hand is that it’s challenging to understand ahead of time when the inflection point of outperformance for Equal Weight will happen. Historically, we have actually seen that turning points have actually accompanied extremes in mega-cap outperformance

We can imagine this relationship by ranking the months in our database by the 12-month relative efficiency of the S&P 500 Leading 50 and dividing them into deciles. Next, we evaluate the average subsequent 12-month efficiency of Equal Weight in each of these deciles. We observe that lower decile S&P 500 Leading 50 months tended to be followed by Equal Weight outperformance in the next year, while greater deciles tended to be followed by Equal Weight underperformance. Presently, thanks to the supremacy of the Stunning 7

stocks, we are at high levels of mega-cap outperformance relative to history, with the S&P 500 Leading 50 exceeding the S&P 500 by 9% in the 12 months through October, beyond the 10 th decile by a margin of 2%. Historically, we have actually seen that a retreat towards a lower decile tended to follow, accompanied by Equal Weight outperformance. Whether we experience a pullback in mega-cap strength or an extension in mega-cap momentum stays to be seen. 1 Efficiency since Nov. 17, 2023.

The posts on this blog site are viewpoints, not recommendations. Please read our Disclaimers

Tags 2023,